Changes in Commercial Leasing Outlook in India 2021 from Q1 to Q2 - Bhutani Group

The leasing outlook in India 2021 from Q1 to Q2 has slowed, following the second wave of the pandemic and resultant lockdowns throughout the country.

Pan India gross leasing stood at 9.9 msf for this quarter, marking 16.9% lower on a q-on-q basis. It stood at 11.93 msf in Q1.

Let’s look at some of the trends that were relevant over Q2 of the year.

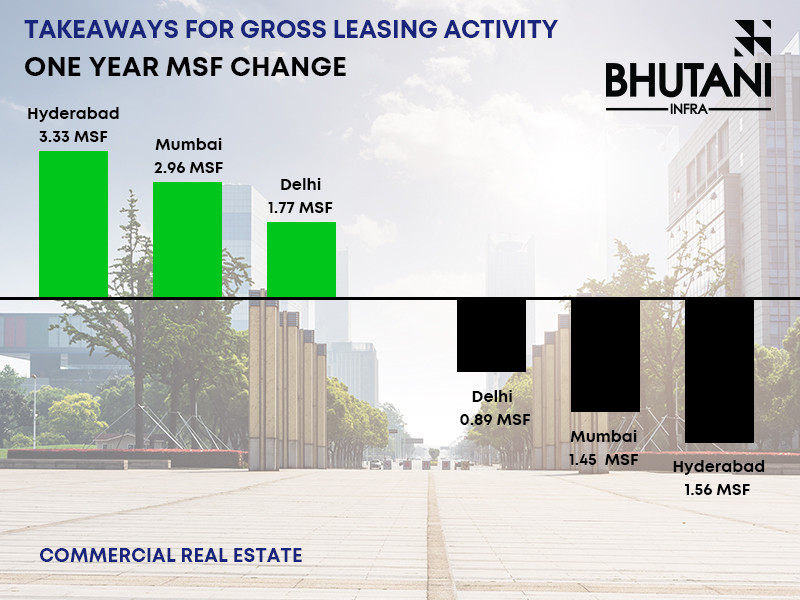

Gross Leasing Activity

The top eight cities recorded a marginal decline (16.9%) in Q2 in terms of gross leasing.

The quarter started on a positive note but the advent of the second COVID-19 wave halted any signs of a speedy recovery in April-May ’21. Here are some takeaways for Gross Leasing Activity that are recorded on the basis of analyzing real estate companies:

- Hyderabad saw the biggest gain in terms of absolute msf leased in Q2 at 3.33 msf. This is a sharp rise from 1.56 msf in Q1 ’21.

- Mumbai perhaps saw the sharpest fall. From 2.96 msf in Q1 to 1.45 in Q2 ’21.

- Delhi too fell from 2.05 msf in Q1 to 1.77 msf in Q2. However, it did 0.89 msf in the same quarter last year.

- Pre-leasing picked up significantly in the quarter, accounting for nearly 31.6% of leasing volumes.

- Organizations are coming back and are looking to take advantage of the market-friendly scenario.

Term Renewals

The second wave and the gradual opening of the offices' posts have left occupiers more concerned with optimizing apex and streamlining costs. Term renewals stood at 2.24 msf in Q2 accounting for around 23% of gross leasing property volume.

Delhi-NCR witnessed a higher number of term renewals, followed by Mumbai.

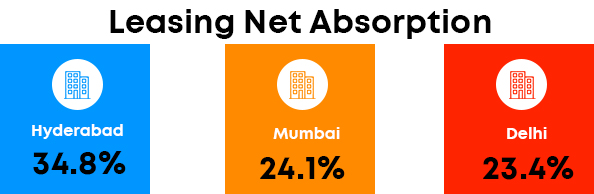

Net Absorption

The category saw a 28% q-on-q growth in Q2 and stood at 4.26 msf. It is 28% higher than Q1 ’21 (3.32 msf) and 28.7% higher than Q2 2020 figure. This can be attributed to pre-commitments becoming operational in the said quarter.

Hyderabad, Mumbai, and Delhi were the biggest names regarding net absorption, with shares of 34.8%, 24.1%, and 23.4% respectively.

Bengaluru recorded 1.48 msf net absorption in Q2 as opposed to 1.61 msf in Q1. The absorption levels will remain low, but it is looking to gain traction.

Occupier Trend

In terms of occupier trends, Engineering & Manufacturing accounted for the highest share of 38.4% in overall leasing. This category is followed by IT-BPM at 21.5%.

Q2 also saw the return of flexible workspaces with healthy corporate demand fuelling this category.

- The number of flexible seats leased reached 31,538 by the end of H1 2021, nearly 87% of the seats leased during the whole of 2020 (36,255).

- Pune and Bengaluru led the way in terms of the absolute number of flexible work seats.

- Hyderabad saw the most significant jump when it came to this category.

With the recent listings of leasing outlook in India 2021, REITs are projected to boost developers’ ability and desire to create more commercial real estate projects, resulting in increased liquidity inflows into the commercial real estate asset class.

Existing lease collections remained largely intact, with no significant difficulty in collecting the billed rentals.

The situation after this Unlock is different since offices will continue to operate following immunization, and they will be more likely to follow COVID protocol to avoid further business interruptions

Leave a comment

All fields marked with an asterisk (*) are required